Aug 2, 2026

July 2026 Market Commentary

Stocks trended sideways for the month, as confidence in sustained advances from AI wavered. The S&P 500 ended the month at 7489, ten (10) points below where it began the month at 7499. The reality of a more protracted conflict in the Middle East may also be sinking in.

Meanwhile, fixed income (i.e. bond) investors grew more skeptical during the month concerning the prospects for inflation. Federal Reserve Chair Kevin Warsh also earned a vote of no confidence at the Fed’s Meeting last week. The Fed held rates steady, but three (3) members (in a 9 to 3 vote) dissented, voting to raise rates.

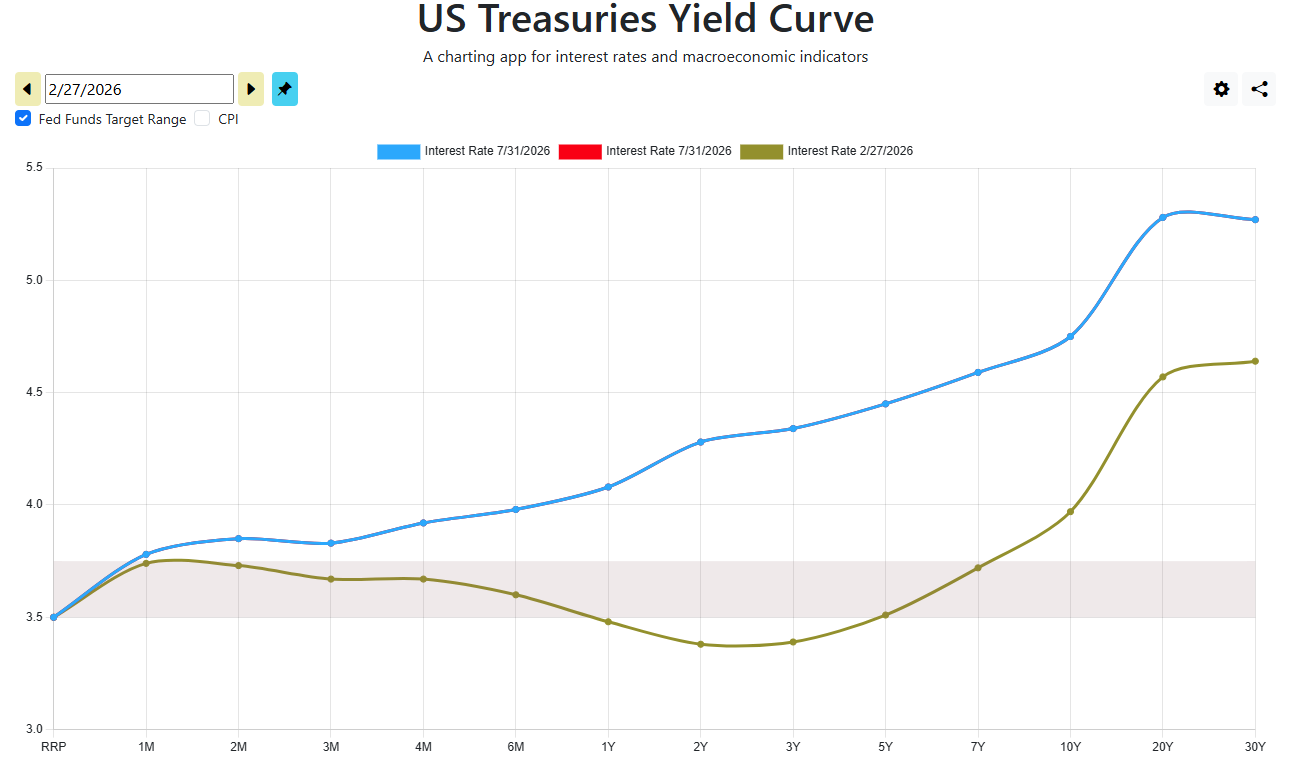

For 2026 as a whole, the yield curve (bond yields, measured by maturities, from overnight to 30-year rates) has trended up. For much of the curve by 25 – 80+ basis points (hundreds of 1%). While the Fed holds rates steady (at last week’s meeting) from 3.5% – 3.75%, the market has already sold off short-term bonds, pushing yields up to 3.8% for 1-month notes, to 4.08% for 1 year and 4.28% for 2-year maturities. In effect, the market has decided that the Fed is acting too slowly, and now forecasts rates in the 4% – 4.25% range within a year or two.

This stands in contrast to the outlook at the beginning of the year, when 2-year US Treasuries yielded just 3.47%. So, to be exact, the 2-year Treasury has increased its yield by 81 bps (basis points) in just the past seven (7) months! Rates were actually trending downward for the first two months of the year, until the start of the Iran War. On Feb 28 the yield on the 2-Year US Treasury stood at just 3.38%. On Friday it was up 90 bps (basis points) to 4.28%.

Similar trends can be observed with the important 10-year US Treasury Bond. Here, yields now stand at 4.75%, up a substantial 31 bps (basis points) from 4.44% on June 30, and up 57 bps (basis points) from 4.18% on January 1. To the average person these seem to be arcane developments. In fact, the Yield Curve is used as the benchmark for credit card rates, auto loan rates, and mortgages. As a result, accelerating inflation and a rising yield curve are flashing warning lights for the economy ahead.

Rising yields also increase the cost that the government must pay to finance ongoing debt spending. Debt service crowds out available funds for programs such as Social Security, Medicare, and Defense. At roughly $1 Trillion in 2026, debt service now costs more than the US Defense Budget, estimated at $895 – $960 Billion. The United States enjoyed low inflation averaging 1.5% from 1990 to 2020. We may now be exiting that benign period and be facing inflation more like that from the late 1960s to the mid-1980s.

Source: ustreasuryyieldcurve.com

July 2, 2026

June 2026 Market Commentary

Stocks trended downward slightly during June, despite the improving situation in the Middle East. The S&P 500 declined from a YTD gain of 10.7% in May to a 9.5% gain by the end of June. The key issue was increasing concern and skepticism over the value of the “Magnificent Seven” stocks (Alphabet, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla) and valuations for AI stocks.

The NASDAQ Composite declined by about 5% pts. in June, while mid-cap and especially small-cap stocks showed healthy gains, indicating rotation out of tech stocks and a broadening of stock ownership beyond the largest corporations. These gains were reflected by an increase of about 3% pts. for the Russell 2000 Index, which includes not just the largest 500 stocks in the market, but 2000 top stocks which includes not just large cap but also mid-and-small-cap equities.

Meanwhile, fixed income (i.e. bonds) moved mostly sideways. Although oil prices came down during the month, inflation is believed to remain an ongoing issue for the balance of the year, albeit less acute of a risk than forecasted a month ago. The President got his new Fed Chief, who declined to cut rates at his first Fed meeting. Meanwhile, expectations remain that rates will go up by a quarter point before 2026 comes to a close. Nonetheless, the bond market took things in stride as at least two rate increases were expected a month or two ago.

With stocks having tripled in value in the past five years valuations, especially those of tech and AI stocks, remain elevated. Increasingly, the market seems to be recognizing this fact.

May 31, 2026

May 2026 Market Commentary

Equities continued to advance strongly in May, driven by healthy earnings, with little concern over the unresolved War with Iran. Excitement continues to grow with the near-term IPOs (Initial Public Offerings) of firms such as SpaceX, Anthropic, and OpenAI. The S&P 500 advanced to a YTD gain of 10.7% by May 29, up from 5.3% in April.

Meanwhile, the bond market took a more sober view. Yields spiked in mid-month, and have come down as May came to a close, but remain somewhat higher (yields move inversely to price) from where they began the month. The Aggregate US Bond Market ended the month about where it started.

Bond investors often take a more sober view than stock pundits, and some argue a more realistic view. The question also comes up increasingly about whether we are in a bubble for stocks. The tech sector now holds 52% of the market capitalization of the entire S&P 500 (compared to 8.3% for healthcare). Meanwhile, the IPOs of SpaceX, Anthropic, and OpenAI suggest this imbalance will grow even more acute.

Consider than during the “dot com” boom of 1999 & 2000 companies such as Sun Microsystems had Price-to-Sales ratios of 10. In contrast, the expected Price-to-Sales ratio for the coming SpaceX IPO is expected to be close to 93 times sales. Meaning an investor buying SpaceX stock would have to wait 93 years to earn back their investment, if SpaceX had zero expenses, zero research and development, and zero payroll. Stocks outside of technology may be fairly priced, but it is hard to ignore the possibility of a bubble for tech stocks, and the overall market equity indices.

May 1, 2026

April 2026 Market Commentary

Markets recovered dramatically, and somewhat surprisingly, in April despite the ongoing war in Iran. Deciding whether investors are extremely savvy, or complacent, is a hard choice. The fact that there has been a cease fire is clearly a factor, but does not fully explain the bullish outlook while oil remains well over $100 per barrel, inflation is accelerating to the 4% range, and global stockpiles of oil, gasoline, diesel, and jet fuel are projected to run out within the next month. Such a development could lead to a further spike in oil prices, and drive inflation throughout the global economy for the balance of 2026.

For the month the S&P 500 surged from a YTD loss of -4.6% in March to a YTD gain of +5.3% by the end of April, to have the best monthly performance since 2020. Global markets also accelerated at a torrid pace, with an increase from -3.9% to +5.2% for the MSCI ACWI (Morgan Stanley All Cap World Index).

Fixed income markets took a different and more pessimistic view, with the US Fixed Income market (as measured by AGG, the iShares US Aggregate Fixed Income Index ETF) softening from a YTD loss of -0.6% in March to -0.8% in April. International Fixed Income (as measured by IAGG, the iShares Global Aggregate Fixed Income Index ETF) moved in sympathy from +0.1% to -0.2% YTD. The key factor being an increase in bond yields as inflation threatens bondholders who now demand higher yields.

The contrasting viewpoint between fixed income and equities is interesting. Declines in fixed income are closer to what most observers would probably have foreseen a month or two ago. At least one observer noted that most Wall Street Professionals are now young enough to have no recollection of events such as inflation of the 1970s, the stock market crash of 1987, the Asian Financial Crises of the late 90s, the Dot Bomb crash of 2000, and even the 2008 Financial Crises. Having come of age over the past two decades when market selloffs usually lead to a quick rebound and a “buy the dip” mentality, perhaps the reaction of the stock market is not a surprise, though one that could be ignoring potentially negative outcomes.

For now, there seems to be little chance of a quick resolution to the War with Iran. Some pundits are now referring not to TACO (Trump Always Chickens Out) but NACHO (Not A Chance that Hormuz Opens). If oil remains well over $100 per barrel for a protracted period and possibly spikes as global stockpiles of fuel evaporate, can markets continue to surge upward? Those with a long-term investment time horizon may be able to ignore these risks and stay fully invested. Those with a shorter-term horizon may be well advised to remain vigilant.

April 5, 2026

March 2026 Market Commentary

Markets in March can be summed up in one word. Uncertainty. The ongoing war in Iran and uncertainty introduced by it put the market into the realm of the unknown during the month. Questions arose as to whether the war would end? When? And with what outcomes? The key variable affecting the global economy and securities prices is, of course, the price of oil. Major price increases from the mid-60s range before the war to prices to as high as $112 per barrel drove major increases for gas prices, concerns that inflation is now accelerating to over 4% per year, and knock on effects that will cause price increases for food, transportation, goods production, and in general price increases throughout the economy. Expectations have gone from 1-2 rate cuts in 2026 to steady rates or even 1-2 rate increases.

Even a resolution of the conflict could result in long-term unknowns. If the USA simply declares victory and walks away will Iran continue to threaten shipping through the Strait of Hormuz? Will oil prices subside, or head to unprecedented levels? Some observers have suggested that oil prices could increase to $150 per barrel, or perhaps even $200 – $300 per barrel, if the USA walks away from the conflict. Implying that the USA may be stuck in a quagmire from which it cannot extract itself. Either way there could be protracted uncertainty, sustained ongoing inflation, and economic unknowns for an extended period-of-time.

Risk-tolerant investors with longer investment horizons may see current prices as an opportunity to jump back into the markets after a quick correction. More risk-averse investors may wish to stay on the sidelines, or only dip their toes into the market and proceed more carefully. In any event, the market seems to be holding on to an optimistic outlook and not yet adopted the view that things could get much worse from here. If sentiment does grow more negative as the conflict and uncertainty drags on, declines could ensue. In any event, markets could continue to be volatile, with major declines or gains. Investors remaining in the markets or buying in at this level should be prepared to stay invested for an extended timeframe to offset the risk of near-term volatility.

February 28, 2026

February 2026 Market Commentary

US Equities continued to be range-bound for the month. Since January 1st the S&P500 has moved sideways, stuck in a range from 6800 to 7000. Fears over the valuations of AI stocks continue to grow, introducing downward pressure on stocks in the near-term. Meanwhile, today’s attack by the United States on Iran introduces significant uncertainty, and could have negative repercussions on stock valuations if the war spreads throughout the Middle East and world oil supplies are threatened.

Meanwhile, International Equities continue to advance. The MSCI ACWI (Morgan Stanley Capital Investment All Cap World Index) increased its YTD gains from 2.2% in January to 2.8% by Feb. 27.

Fixed Income has benefitted as capital seeks a “safe haven.” The US 10 Year Treasury saw its yield decline from a peak of 4.28% on Feb 2 to 3.95% on Feb 27. A dramatic decline in one month of 33 basis points. Remember, bond yields move inversely to price. The decline in the 10 Year Yield below 4% helped push mortgage rates below 6% for the first time since 2022.

In the near-term, with uncertainty over AI, and a new war in Iran, caution is warranted. There is no compelling near-term driver to move stocks higher, while at least a minor self-off of 5% is likely in early 2026. International stocks continue to provide the best option in the near-term. In the US, small and mid-cap stocks, as well as dividend-oriented stocks, are more compelling at this juncture vs large cap equities.

Peter Gaylord, CFA

Gaylord Wealth Management, LLC

Rocklin, CA